Note

This tutorial is available as a Jupyter notebook. Download notebook

Tutorial 11: Sample Weighting#

🟡 Intermediate — Familiarity with ML concepts helpful

Learn how to use sample weights to handle class imbalance, emphasize recent data, and downweight outliers.

What you’ll learn#

Handle class imbalance with balanced sample weights

Use temporal weighting for concept drift

Downweight outliers and noisy samples

Integrate sample weights with both sklearn and core APIs

[1]:

import numpy as np

from sklearn.datasets import make_classification

from sklearn.metrics import classification_report

from sklearn.model_selection import train_test_split

from sklearn.utils.class_weight import compute_sample_weight

import boosters

from boosters.sklearn import GBDTClassifier, GBDTRegressor

Why Sample Weights?#

Sample weights allow you to control how much each training example contributes to the model:

Class imbalance: Give minority class samples higher weights

Temporal importance: Weight recent data more heavily for concept drift

Data quality: Downweight known outliers or noisy samples

Business logic: Emphasize high-value customers or critical cases

1. Handling Class Imbalance#

When classes are imbalanced, the model tends to favor the majority class. Sample weights can correct this by giving minority samples more importance.

[2]:

# Create imbalanced dataset (95% class 0, 5% class 1)

rng = np.random.default_rng(42)

n_samples = 1000

n_minority = 50

X = rng.standard_normal((n_samples, 5)).astype(np.float32)

# Create imbalanced labels

y = np.zeros(n_samples, dtype=np.float32)

y[:n_minority] = 1.0

# Shuffle

perm = rng.permutation(n_samples)

X, y = X[perm], y[perm]

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=42, stratify=y

)

print(f"Class distribution in training: {np.bincount(y_train.astype(int))}")

print(f"Class distribution in test: {np.bincount(y_test.astype(int))}")

Class distribution in training: [760 40]

Class distribution in test: [190 10]

Without Sample Weights#

The model will likely predict only the majority class:

[3]:

clf_no_weights = GBDTClassifier(n_estimators=50, verbose=0)

clf_no_weights.fit(X_train, y_train)

pred_no_weights = clf_no_weights.predict(X_test)

print("Classification Report (no weights):")

print(classification_report(y_test, pred_no_weights, zero_division=0))

Classification Report (no weights):

precision recall f1-score support

0.0 0.95 1.00 0.97 190

1.0 0.00 0.00 0.00 10

accuracy 0.95 200

macro avg 0.47 0.50 0.49 200

weighted avg 0.90 0.95 0.93 200

With Balanced Sample Weights#

sklearn’s compute_sample_weight calculates weights inversely proportional to class frequency:

[4]:

# Compute balanced weights

weights = compute_sample_weight("balanced", y_train)

print(f"Weight for class 0 samples: {weights[y_train == 0][0]:.3f}")

print(f"Weight for class 1 samples: {weights[y_train == 1][0]:.3f}")

print(f"Ratio: {weights[y_train == 1][0] / weights[y_train == 0][0]:.1f}x")

Weight for class 0 samples: 0.526

Weight for class 1 samples: 10.000

Ratio: 19.0x

[5]:

clf_weighted = GBDTClassifier(n_estimators=50, verbose=0)

clf_weighted.fit(X_train, y_train, sample_weight=weights)

pred_weighted = clf_weighted.predict(X_test)

print("Classification Report (with balanced weights):")

print(classification_report(y_test, pred_weighted, zero_division=0))

Classification Report (with balanced weights):

precision recall f1-score support

0.0 0.95 0.93 0.94 190

1.0 0.00 0.00 0.00 10

accuracy 0.89 200

macro avg 0.47 0.47 0.47 200

weighted avg 0.90 0.89 0.89 200

2. Temporal Weighting for Concept Drift#

When data distribution changes over time (concept drift), you may want to emphasize recent observations. This is common in:

Financial markets

User behavior prediction

Fraud detection

[6]:

# Simulate temporal data with concept drift

rng = np.random.default_rng(42)

n_samples = 500

X = rng.standard_normal((n_samples, 3)).astype(np.float32)

# Target relationship changes over time:

# Early: y depends mostly on X[:, 0]

# Late: y depends mostly on X[:, 1]

time_factor = np.linspace(0, 1, n_samples)

y = ((1 - time_factor) * X[:, 0] + time_factor * X[:, 1]).astype(np.float32)

y += rng.standard_normal(n_samples).astype(np.float32) * 0.1

# Split chronologically (not randomly!)

train_size = 400

X_train, X_test = X[:train_size], X[train_size:]

y_train, y_test = y[:train_size], y[train_size:]

print(f"Training on first {train_size} samples")

print(f"Testing on last {n_samples - train_size} samples (most recent)")

Training on first 400 samples

Testing on last 100 samples (most recent)

[7]:

# Uniform weights baseline

reg_uniform = GBDTRegressor(n_estimators=50, verbose=0)

reg_uniform.fit(X_train, y_train)

pred_uniform = reg_uniform.predict(X_test)

rmse_uniform = np.sqrt(np.mean((pred_uniform - y_test) ** 2))

# Exponential decay weights - recent samples have higher weight

decay_rate = 3.0 # Higher = more emphasis on recent data

temporal_weights = np.exp(decay_rate * np.linspace(0, 1, train_size)).astype(np.float32)

reg_weighted = GBDTRegressor(n_estimators=50, verbose=0)

reg_weighted.fit(X_train, y_train, sample_weight=temporal_weights)

pred_weighted = reg_weighted.predict(X_test)

rmse_weighted = np.sqrt(np.mean((pred_weighted - y_test) ** 2))

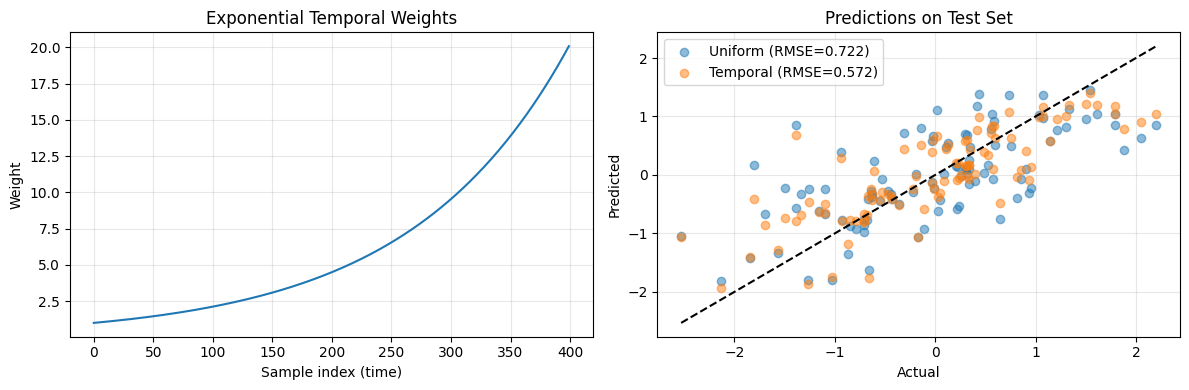

print(f"RMSE with uniform weights: {rmse_uniform:.4f}")

print(f"RMSE with temporal weights: {rmse_weighted:.4f}")

print(f"Improvement: {(rmse_uniform - rmse_weighted) / rmse_uniform * 100:.1f}%")

RMSE with uniform weights: 0.7219

RMSE with temporal weights: 0.5716

Improvement: 20.8%

[8]:

import matplotlib.pyplot as plt

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(12, 4))

# Plot weight distribution

ax1.plot(temporal_weights)

ax1.set_xlabel("Sample index (time)")

ax1.set_ylabel("Weight")

ax1.set_title("Exponential Temporal Weights")

ax1.grid(True, alpha=0.3)

# Plot predictions vs actual

ax2.scatter(y_test, pred_uniform, alpha=0.5, label=f"Uniform (RMSE={rmse_uniform:.3f})")

ax2.scatter(y_test, pred_weighted, alpha=0.5, label=f"Temporal (RMSE={rmse_weighted:.3f})")

ax2.plot([y_test.min(), y_test.max()], [y_test.min(), y_test.max()], "k--")

ax2.set_xlabel("Actual")

ax2.set_ylabel("Predicted")

ax2.set_title("Predictions on Test Set")

ax2.legend()

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

3. Downweighting Outliers#

If you know certain samples are outliers or noisy, you can reduce their influence:

[9]:

rng = np.random.default_rng(42)

X = rng.standard_normal((200, 4)).astype(np.float32)

y = (X[:, 0] + X[:, 1] * 0.5 + rng.standard_normal(200) * 0.1).astype(np.float32)

# Inject some outliers

outlier_idx = [10, 50, 100, 150]

y[outlier_idx] = y[outlier_idx] + 10.0 # Shift by 10 standard deviations

# Create weights - downweight outliers

weights = np.ones(200, dtype=np.float32)

weights[outlier_idx] = 0.01 # Very low weight for known outliers

print(f"Number of outliers: {len(outlier_idx)}")

print(f"Outlier weight: {weights[outlier_idx[0]]}")

Number of outliers: 4

Outlier weight: 0.009999999776482582

[10]:

# Without outlier handling

reg_no_handling = GBDTRegressor(n_estimators=50, verbose=0)

reg_no_handling.fit(X, y)

pred_no_handling = reg_no_handling.predict(X)

# With outlier downweighting

reg_downweight = GBDTRegressor(n_estimators=50, verbose=0)

reg_downweight.fit(X, y, sample_weight=weights)

pred_downweight = reg_downweight.predict(X)

# Calculate RMSE on non-outlier samples only

mask = ~np.isin(np.arange(len(y)), outlier_idx)

rmse_no = np.sqrt(np.mean((pred_no_handling[mask] - y[mask]) ** 2))

rmse_dw = np.sqrt(np.mean((pred_downweight[mask] - y[mask]) ** 2))

print(f"RMSE on clean samples (no handling): {rmse_no:.4f}")

print(f"RMSE on clean samples (with weights): {rmse_dw:.4f}")

RMSE on clean samples (no handling): 0.2987

RMSE on clean samples (with weights): 0.1037

4. Core API with Sample Weights#

You can also use sample weights directly with the core Dataset and GBDTModel API:

[11]:

from boosters import Dataset, GBDTConfig, GBDTModel, Objective

rng = np.random.default_rng(42)

X = rng.standard_normal((200, 4)).astype(np.float32)

y = (X[:, 0] + X[:, 1] * 0.5 + rng.standard_normal(200) * 0.1).astype(np.float32)

# Create custom weights

weights = np.ones(200, dtype=np.float32)

weights[np.abs(y) > 2] = 0.1 # Downweight extreme values

print(f"Samples with reduced weight: {np.sum(weights < 1)}")

Samples with reduced weight: 17

[12]:

# Create dataset WITH weights

train_data = Dataset(

X, y,

weights=weights,

feature_names=["feat_a", "feat_b", "feat_c", "feat_d"]

)

config = GBDTConfig(

n_estimators=50,

max_depth=4,

learning_rate=0.1,

objective=Objective.squared(),

)

model = GBDTModel.train(train_data, config=config)

predictions = model.predict(Dataset(X))

rmse = np.sqrt(np.mean((predictions.flatten() - y) ** 2))

print(f"Training RMSE: {rmse:.4f}")

print(f"Feature names stored in model: {model.feature_names}")

Training RMSE: 0.2142

Feature names stored in model: ['feat_a', 'feat_b', 'feat_c', 'feat_d']

Summary#

Sample weights are a powerful tool for:

Use Case |

Weight Strategy |

|---|---|

Class imbalance |

Inverse class frequency ( |

Concept drift |

Exponential decay (recent → higher weight) |

Known outliers |

Low fixed weight (e.g., 0.01) |

Business importance |

Custom weights per sample |

Key Points#

sklearn API: Pass

sample_weightto.fit()Core API: Pass

weightstoDataset()Weights are relative — they don’t need to sum to 1

Use

compute_sample_weight("balanced")for quick class balancingFor temporal weighting, use exponential decay:

exp(rate * normalized_time)

Next Steps#

Tutorial 07: Hyperparameter Tuning — Optimize model performance

Tutorial 08: Explainability — Understand model predictions

User Guide: Recipes — Common patterns and solutions